I wrote two entries towards the end of 2015 about slowing down (a.k.a. work-life balance) and de-cluttering.

Enter 2016 + Chinese New Year spring cleaning. Spring cleaning this year it is a big affair because I am moving house, so almost every corner of my house gets packed.

Here’s the top three surprises I’ve found in my home:

- There are more kitchen appliances than you can ever imagine. The kitchen already has a hob and a built-in oven, but then there’s also an air fryer, mini toaster oven, microwave oven, juice blender, food blender, handheld blender (for baking?), pots, pans, more pots, even more pans, tea sets, even more tea sets (I don’t even drink tea, so they have been in storage for eons), dozens of cups/mugs/salt+pepper shakers from events or weddings.

- There’s more gadgets than you can ever use in a day. Air filters. Fans. Radio… speakers… more speakers big and small. Earphones/headphones… lots of them. Old MP3 players, iPods, old iPhones, iPads, cameras. USB cables, power cables, even more USB cables. TVs — two of them. Ugh!

- There’s more cleaning products/gadgets than you ever need. Vacuum cleaners, steam cleaners (this was really a bad purchase on my part), traditional mop, high-tech 3M mop. Long brush, short brush, big brush, small brush, weird shape brush. Febreeze, Dettol, Lysol, Clorox, 3M and about a dozen other cleaning solutions.

It’s NUTS! All the crap I bought. All the things I was made to believe work wonders when in fact all I really needed was probably a third or less of those. I sold/donated/threw a bunch of stuff away, and it was really hard to make some of those decisions, but I had to because the harder the decision, the stronger the memory. I am also making it a point to blog about this so I will never repeat the same mistakes.

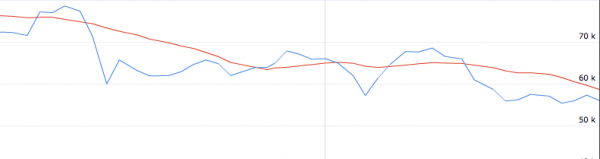

But what really surprised me was my OCD tendency to keep track of all my bank statements, bills and other documents. To my surprise, I have every single one of my bank statements since 2007. Looking back at them reminds me of my past, and tells a better story than I can even recall myself:

I was living paycheck-to-paycheck back in 2007 and had close to no savings. I had maybe several hundred dollars balance at the end of every month (and it never grew). I remember I would look at my bank statements and make a note beside every transaction trying to figure out what it was for or where I spent my money, but a large bulk of it would be cash withdrawals at the ATM, so it was not clear if it was food, fancy restaurant meals (did not have credit card back then), cab fares or maybe even shopping.

The turning point was when I started tracking my expenses in detail. Having an iPhone 3G (2008) and an app was key. I tracked close to every single cent I spent and saw that food expenses made up around $600/month. I tried to reduce, but it was hard because I worked in CBD, and food was (is) generally expensive. I also ate out most of the time — including dinner. My transport expenses were also high, because I occasionally cab or drive to work and had to pay crazy parking rates in town.

I switched jobs in 2008. I worked outside of CBD but I drove to work daily and still had to pay for pretty expensive parking (averaging around $400/month) because I could not get season parking and had to pay hourly. However, food was cheap and I ate chye png almost every day for lunch and that brought my total expenses down. Together with an increase in salary, I started to see some savings, and with some excess money, I also bought basic life and health insurance.

The rest of the story will be for another day. Anyway, as I flipped through my bank statements, I saw how this similar pattern added on to my savings bit by bit. My income has risen over the years of course, and my lifestyle may have also gotten more expensive, but the key was that my lifestyle expenses grew less than my income, and I think this is really important. Hopefully, an old friend is reading this — YOLO is not the way to go.

I said in an earlier post that I would write about my resolutions for 2016. So here it is.

Be grateful. I am grateful for all the people whom I’ve met along this journey, good or bad because all that has happened made me where I am today. I do hope to continue having more exciting years ahead.

Reduce. Consumerism is scary and it will suck the life out of you. The next time I whip out my credit card, I need to think thrice. As a result, I’ve also reduced all my credit card limits. Banks are really insane these days to give out 4x your monthly salary.

Focus. I had little distractions during the early years of my work life and it allowed me to focus on what I had to do, so I could do it right. I’ve found this very important, and the lack of focus is the reason why a lot of people fail. Not being arrogant but I do get quite a fair bit of “noise” with people approaching me to become a tech co-founder. Do not take offence if I reject you because I can’t do so many things at once; if I were your co-founder, you’d want me to focus on your stuff too.